A record fall in GDP means getting the economy back to where it once was will require an unprecedented haul back

Official confirmation from the ONS that the UK economy was in a recession in the first half of the year should not be a surprise to anybody. As a direct result of the nationwide lockdown between 23 March and mid-May, the economy contracted by 2.2% in the first quarter followed by a record 20.4% fall in the second. Depicted on a chart, the precipitous drop in such a short period of time is remarkable and unlike anything that has happened before.

Of course, a widespread shutdown in activity to contain a global pandemic is new to us all and the full national accounts data provide the clearest picture of how badly different parts of the economy were affected.

April bore the brunt of the downturn, with GDP contracting by 20.0%. This was followed by rises of 2.4% in May and 8.7% in June as lockdown measures were eased

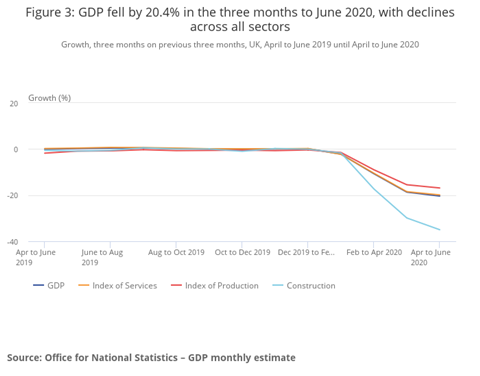

By sector, industrial production declined 16.9%, services fell 19.9% and construction contracted by 35%. Spending by households and investment from businesses also fell by around a quarter and a third respectively. As with the overall GDP figure, these are all record declines.

While these quarterly figures illustrate the extent of the impact of coronavirus on the UK economy, the monthly profile is more revealing. As the only full month with restrictions in place, April bore the brunt of the downturn, with GDP contracting by 20.0%. This was followed by rises of 2.4% in May and 8.7% in June as lockdown measures were eased and more business reopened. Nevertheless, for June, GDP was still 16.8% lower compared with a year earlier and 17.2% below pre-coronavirus levels in February.

An economic shock of this magnitude would typically be accompanied by a deterioration in the labour market, but in response to an unprecedented shutdown there has also been unprecedented support to keep jobs on the payroll through the furlough scheme. For that reason, despite 7.7 million workers recorded as being temporarily away from work in the second quarter and total hours worked falling by 18.4% over the period, headline rates of employment and unemployment have remained largely unchanged.

Early indicators for July suggest that all areas of the economy have continued picking up and there has certainly been much hope of pent-up demand driving the recovery through the summer months, construction included. The big test will be whether it has recovered enough to reabsorb the workers still being furloughed, and particularly once the Coronavirus Job Retention Scheme ends in October.

In mid-July, businesses were reporting that 18.5% of the workforce was still being furloughed. With even the most optimistic forecasts assuming that the economy will take until the end of 2021 to return to its pre-coronavirus levels of output, that adds a new layer of uncertainty and, perhaps, also hints that it will be a recovery like no other.

Rebecca Larkin is senior economist at the Construction Products Association

No comments yet