Construction employment and activity remained downbeat in August, with orders below normal. However, the residential sector provided a chink in the clouds. Experian Economics reports

01 / THE STATE OF PLAY

The seasonally adjusted activity index rose by six points to reach the no-change mark of 50 in August. Activity declined in two of the three sectors in August, although the non-residential activity index edged up by one point to 49 while the civil engineering index rose by five points to reach a three-month high of 46, suggesting weaker rates of decline. In contrast, the residential sector recorded a marked improvement in its activity index, which was in positive territory for the first time in 10 months. The index rose by 14 points to 53, indicating that activity in the sector increased during August.

The tender enquiries index edged down by two points to 50, indicating that tender enquiries remained unchanged during the month, but orders continued to be below normal for the time of year, highlighted by the index remaining below the no-change mark at 46.

Prospects for construction employment over the coming three months remain downbeat, with employment prospects indices across the three sub-sectors still in negative territory. The total employment prospects index edged down to reach a three-month low of 36.

In August, around 24% of respondents indicated that there were no factors constraining activity, falling from July’s three-year high of 29%. More than half (55%) reported that insufficient demand was constraining their activity, slightly higher than in the previous month. Finance was reported as a constraining factor on activity by 17% of respondents, the highest proportion since March.

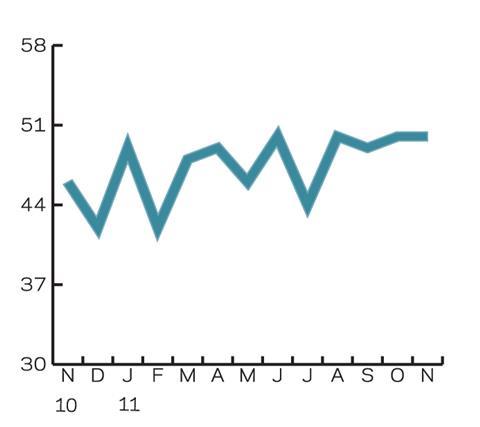

02 / LEADING CONSTRUCTION ACTIVITY INDICATOR

CFR’s Leading Construction Activity Indicator is expected to fall back into negative territory in September, albeit only marginally at 49, before edging up to the no-change mark of 50 in October. It will remain unchanged at this level in November.

The indicator uses a base level of 50: an index above that level indicates an increase in activity, below that level a decrease.

03 / MATERIAL COSTS

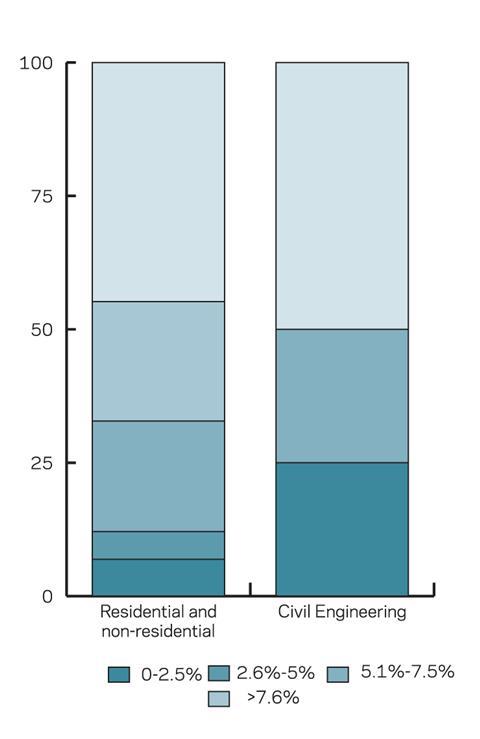

About 45% of building firms reported annual material cost inflation of more than 7.6% in August, lower than the 61% three months ago. The proportion of firms indicating that material costs had fallen since August 2010 also increased, from just 3.4% to almost 7%.

In contrast, the proportion of civil engineering firms indicating strong material cost inflation of more than 7.6% remained unchanged at 50% in August, while 25% of respondents indicated that costs for materials had fallen. This was also unchanged from three months ago.

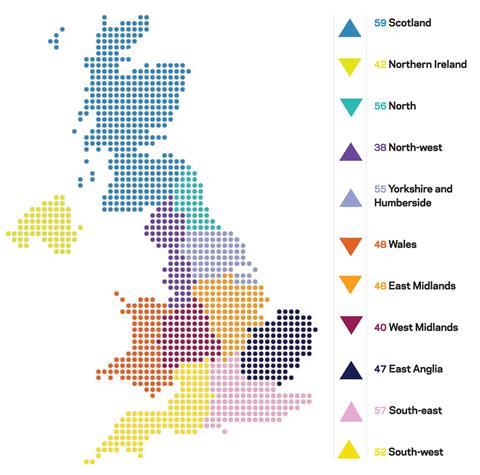

04 / REGIONAL PERSPECTIVE

Experian’s regional composite indices incorporate current activity levels, the state of order books and the level of tender enquiries received by contractors to provide a measure of the relative strength of each regional industry.

Six of the 11 regional indices rose in August. The index for Yorkshire and Humberside saw the strongest increase, rising by four points to a 13-month high of 55. The South-west’s index rose by three points, taking it back into positive territory with 52 points, following two months of below-50 readings. The South-east and Scotland both saw their indices increase by two points, to 57 and 59, respectively.

The indices for East Anglia and the North-west both edged up by one point but remained in negative territory at 47 and 38, respectively.

The biggest fall was in the Northern Ireland index, which declined by four points to 42, its lowest reading for eight months. The East Midlands and Welsh indices fell by three points, both dropping below the no-change mark to 48.

The index for the North remained in positive territory for a third successive month, although the index edged down by two points to 56. The West Midlands’ index was also two points lower at 40.

The index for the UK, which includes firms working in five or more regions, rose by two points to 55.

No comments yet